Starting a small business when you have bad credit can feel daunting. With lower personal credit scores, securing financing to launch and grow your company can be tough. However, there are solutions if you stay determined. This guide examines the legal implications of bad credit for entrepreneurs and provides actionable tips to improve your financial standing.

For people who want to start their own businesses but have bad credit, it’s hard to get money to make their business grow. But don’t worry! With some determination and the right help, there are ways to move forward.

Low credit scores can cost you over $100,000 more for a mortgage. This article looks at how having bad credit can affect small businesses legally and gives practical tips to make your money situation better.

Recent credit score statistics show approximately 40% of Americans have subprime credit scores under 670. This makes obtaining financing difficult for many aspiring business owners who rely on personal credit initially. Missed payments and irresponsible borrowing can also jeopardize professional goals like renting office space or getting a cell phone contract.

The effects of negative marks on your credit history are far-reaching. Beyond being denied loans, bad credit leads to higher interest rates, larger deposits, and more fees for services. Credit repair takes time, but developing good financial habits now can reap rewards for your entrepreneurial endeavors down the road.

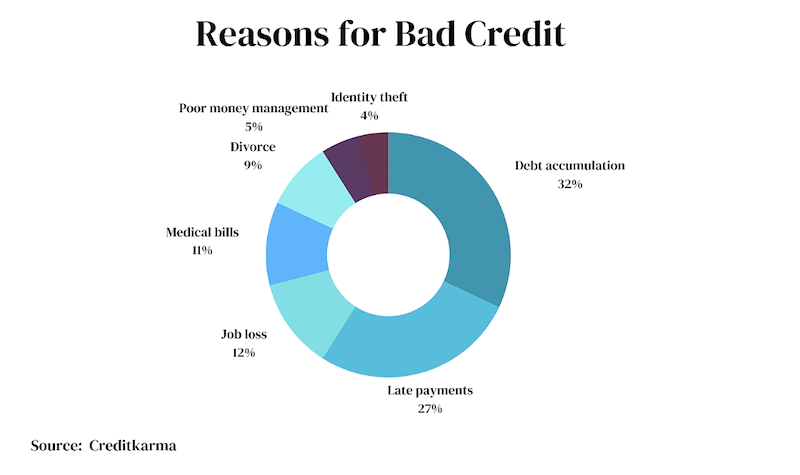

How Bad Credit Impedes Small Business Progress

According to an annual survey by the Consumer Federation of America and VantageScore Solutions, 43% of consumers haven’t checked their credit scores in the last year. Missed payments and irresponsible borrowing habits can make everything from securing a cell phone contract to renting an apartment more challenging.

Poor personal credit scores create monumental obstacles for entrepreneurs trying to get their ventures off the ground. Without access to capital, viable business ideas remain just that – ideas.

Traditional lending sources like banks rely heavily on credit scores to approve financing. They view bad credit applicants as high risk and deny them. Specific hurdles stemming from low scores include:

? Inability to qualify for small business loans or lines of credit to cover expenses.

? Struggles to find angel investors willing to provide startup funding.

? Difficulty getting approved for a business credit card to build a credit history.

? Challenges renting physical retail space for a storefront location.

? Paying higher merchant account processing fees due to perceived risk.

? Limited financing options for purchasing commercial vehicles, equipment, hardware, or software.

? The necessity of paying large utility deposits before activating essential services.

Each of these obstacles caused by poor credit can completely derail progress on launching or scaling a company. Having access to working capital is the lifeblood of any successful venture. Without it, entrepreneurs cannot cover essential upfront costs associated with turning vision into reality.

The Ongoing Financial Strain of Bad Credit

Beyond simply being denied financing, bad credit has compounding effects that permeate every area of personal and business finances. Low scores lead to:

? Significantly higher interest rates on credit cards, auto loans, and mortgages.

? Larger security deposits and processing fees are required by lenders and service providers.

? Challenges obtaining basic utilities like electricity, gas, and phone service without paying deposits.

? Difficulty qualifying for apartment rentals or home mortgages, resulting in extra fees.

? Increased insurance premiums for home, auto, health, and business policies.

? Restrained access to new credit cards and personal loans due to limited approval odds.

? Restrictions on student loan amounts are offered based on low creditworthiness.

These elevated rates and costs quickly drain working capital and cash flow. For entrepreneurs operating on tight margins, the financial burdens imposed by poor credit can become impossible to manage. It leads to a vicious cycle of robbing funds from the business to cover higher payments.

A Gradualist Approach to Credit Repair

Improving poor credit takes time, diligence, and an understanding of how to rehabilitate your profile strategically. Proven techniques include:

? Paying all current debts and bills on time to stop further damage

? Paying down balances to lower credit utilization ratios

? Limiting new credit applications to avoid additional hard inquiries

? Disputing any reporting errors with evidence to support your claims

? Exploring credit counseling services to consolidate debt

? Obtaining and responsibly using secured credit cards to demonstrate a positive payment history

With consistent effort over 6-12 months, your score can rise significantly. However, there are no shortcuts, so be patient and focus on establishing healthy long-term habits.

Alternative Funding to Get Your Business Going

As you work to improve your personal credit, some options to secure working capital include:

? Crowdfunding through platforms like Kickstarter and Indiegogo.

? Short-term business loans from alternative online lenders.

? Merchant cash advances based on future sales.

? Federal or private grants.

? Partnerships with those who have better credit.

? Negotiating extended payment terms with vendors.

By tapping into these resources, you can make progress on your entrepreneurial vision while simultaneously rehabilitating your finances. With dedication and the right help, your business aspirations are still achievable even with bad credit. Don’t get discouraged.

The Ongoing Financial Strain of Bad Credit

Beyond simply being denied financing, bad credit has compounding effects that permeate every area of personal and business finances. Low scores lead to:

? Significantly higher interest rates on credit cards, auto loans, and mortgages.

? Larger security deposits and processing fees are required by lenders and service providers.

? Challenges obtaining basic utilities like electricity, gas, and phone service without paying deposits.

? Difficulty qualifying for apartment rentals or home mortgages, resulting in extra fees.

? Increased insurance premiums for home, auto, health, and business policies.

? Restrained access to new credit cards and personal loans due to limited approval odds.

? Restrictions on student loan amounts are offered based on low creditworthiness.

These elevated rates and costs quickly drain working capital and cash flow. For entrepreneurs operating on tight margins, the financial burdens imposed by poor credit can become impossible to manage.

It leads to a vicious cycle of robbing funds from the business to cover higher payments.

Frequently Asked Questions on Bad Credit and Small Business

How does bad credit affect the chances of obtaining a small business loan?

Poor credit significantly reduces the chances of securing financing from traditional lenders who rely heavily on personal credit scores to assess applicant risk and make decisions. Those with low scores will likely need to seek out alternative funding sources.

What are some alternative financing options for small businesses with bad credit?

Options like crowdfunding, short-term business loans from alternative lenders, merchant cash advances, grants, business partnerships, and vendor credit can provide working capital for entrepreneurs unable to obtain traditional small business loans or lines of credit.

How can a small business owner proactively improve their personal credit?

Strategies include paying all bills on time, paying down credit card balances, limiting new credit applications, correcting any errors on credit reports, considering credit counseling services, and demonstrating responsible usage of any new lines of credit obtained. Legal assistance can also help dispute issues.

Should business credit be built separately from personal credit?

Yes, establishing business credit separately creates a credit profile based on the company’s financial track record, rather than the owner’s personal score. This can help improve the chances of loan approval.

How long does it take to recover from bad credit?

Typically it takes at least 6 months of diligent financial management to see significant improvement in your credit score. It takes time to rebuild a positive payment history and lower credit utilization. Bankruptcies can impact scores for up to 10 years.

Even though it’s not easy, small business owners can do things to fix bad credit find alternative ways to get the money they need, and pursue alternative funding options to turn their entrepreneurial aspirations into reality. With persistence and diligence, financial recovery is possible.